[ad_1]

Time-series forecasting is an important research area that is critical to several scientific and industrial applications, like retail supply chain optimization, energy and traffic prediction, and weather forecasting. In retail use cases, for example, it has been observed that improving demand forecasting accuracy can meaningfully reduce inventory costs and increase revenue.

Modern time-series applications can involve forecasting hundreds of thousands of correlated time-series (e.g., demands of different products for a retailer) over long horizons (e.g., a quarter or year away at daily granularity). As such, time-series forecasting models need to satisfy the following key criterias:

- Ability to handle auxiliary features or covariates: Most use-cases can benefit tremendously from effectively using covariates, for instance, in retail forecasting, holidays and product specific attributes or promotions can affect demand.

- Suitable for different data modalities: It should be able to handle sparse count data, e.g., intermittent demand for a product with low volume of sales while also being able to model robust continuous seasonal patterns in traffic forecasting.

A number of neural network–based solutions have been able to show good performance on benchmarks and also support the above criterion. However, these methods are typically slow to train and can be expensive for inference, especially for longer horizons.

In “Long-term Forecasting with TiDE: Time-series Dense Encoder”, we present an all multilayer perceptron (MLP) encoder-decoder architecture for time-series forecasting that achieves superior performance on long horizon time-series forecasting benchmarks when compared to transformer-based solutions, while being 5–10x faster. Then in “On the benefits of maximum likelihood estimation for Regression and Forecasting”, we demonstrate that using a carefully designed training loss function based on maximum likelihood estimation (MLE) can be effective in handling different data modalities. These two works are complementary and can be applied as a part of the same model. In fact, they will be available soon in Google Cloud AI’s Vertex AutoML Forecasting.

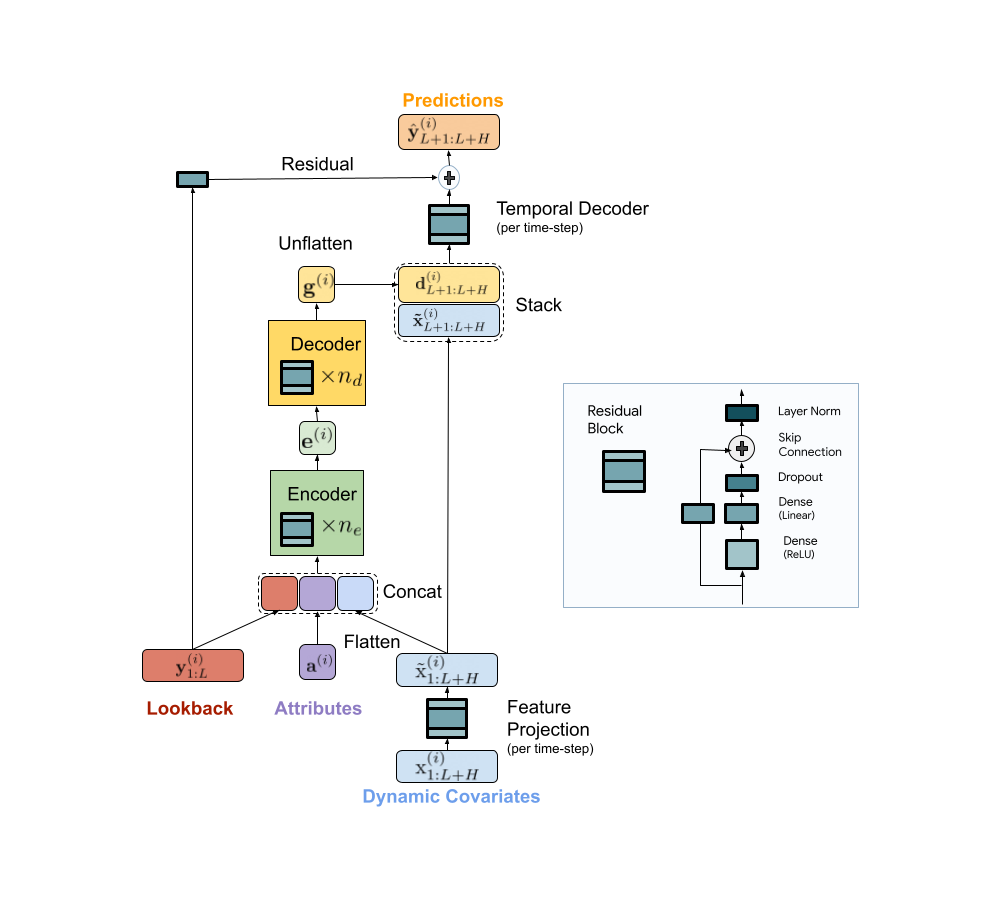

TiDE: A simple MLP architecture for fast and accurate forecasting

Deep learning has shown promise in time-series forecasting, outperforming traditional statistical methods, especially for large multivariate datasets. After the success of transformers in natural language processing (NLP), there have been several works evaluating variants of the Transformer architecture for long horizon (the amount of time into the future) forecasting, such as FEDformer and PatchTST. However, other work has suggested that even linear models can outperform these transformer variants on time-series benchmarks. Nonetheless, simple linear models are not expressive enough to handle auxiliary features (e.g., holiday features and promotions for retail demand forecasting) and non-linear dependencies on the past.

We present a scalable MLP-based encoder-decoder model for fast and accurate multi-step forecasting. Our model encodes the past of a time-series and all available features using an MLP encoder. Subsequently, the encoding is combined with future features using an MLP decoder to yield future predictions. The architecture is illustrated below.

|

| TiDE model architecture for multi-step forecasting. |

TiDE is more than 10x faster in training compared to transformer-based baselines while being more accurate on benchmarks. Similar gains can be observed in inference as it only scales linearly with the length of the context (the number of time-steps the model looks back) and the prediction horizon. Below on the left, we show that our model can be 10.6% better than the best transformer-based baseline (PatchTST) on a popular traffic forecasting benchmark, in terms of test mean squared error (MSE). On the right, we show that at the same time our model can have much faster inference latency than PatchTST.

|

| Left: MSE on the test set of a popular traffic forecasting benchmark. Right: inference time of TiDE and PatchTST as a function of the look-back length. |

Our research demonstrates that we can take advantage of MLP’s linear computational scaling with look-back and horizon sizes without sacrificing accuracy, while transformers scale quadratically in this situation.

Probabilistic loss functions

In most forecasting applications the end user is interested in popular target metrics like the mean absolute percentage error (MAPE), weighted absolute percentage error (WAPE), etc. In such scenarios, the standard approach is to use the same target metric as the loss function while training. In “On the benefits of maximum likelihood estimation for Regression and Forecasting”, accepted at ICLR, we show that this approach might not always be the best. Instead, we advocate using the maximum likelihood loss for a carefully chosen family of distributions (discussed more below) that can capture inductive biases of the dataset during training. In other words, instead of directly outputting point predictions that minimize the target metric, the forecasting neural network predicts the parameters of a distribution in the chosen family that best explains the target data. At inference time, we can predict the statistic from the learned predictive distribution that minimizes the target metric of interest (e.g., the mean minimizes the MSE target metric while the median minimizes the WAPE). Further, we can also easily obtain uncertainty estimates of our forecasts, i.e., we can provide quantile forecasts by estimating the quantiles of the predictive distribution. In several use cases, accurate quantiles are vital, for instance, in demand forecasting a retailer might want to stock for the 90th percentile to guard against worst-case scenarios and avoid lost revenue.

The choice of the distribution family is crucial in such cases. For example, in the context of sparse count data, we might want to have a distribution family that can put more probability on zero, which is commonly known as zero-inflation. We propose a mixture of different distributions with learned mixture weights that can adapt to different data modalities. In the paper, we show that using a mixture of zero and multiple negative binomial distributions works well in a variety of settings as it can adapt to sparsity, multiple modalities, count data, and data with sub-exponential tails.

|

| A mixture of zero and two negative binomial distributions. The weights of the three components, a1, a2 and a3, can be learned during training. |

We use this loss function for training Vertex AutoML models on the M5 forecasting competition dataset and show that this simple change can lead to a 6% gain and outperform other benchmarks in the competition metric, weighted root mean squared scaled error (WRMSSE).

| M5 Forecasting | WRMSSE |

| Vertex AutoML | 0.639 +/- 0.007 |

| Vertex AutoML with probabilistic loss | 0.581 +/- 0.007 |

| DeepAR | 0.789 +/- 0.025 |

| FEDFormer | 0.804 +/- 0.033 |

Conclusion

We have shown how TiDE, together with probabilistic loss functions, enables fast and accurate forecasting that automatically adapts to different data distributions and modalities and also provides uncertainty estimates for its predictions. It provides state-of-the-art accuracy among neural network–based solutions at a fraction of the cost of previous transformer-based forecasting architectures, for large-scale enterprise forecasting applications. We hope this work will also spur interest in revisiting (both theoretically and empirically) MLP-based deep time-series forecasting models.

Acknowledgements

This work is the result of a collaboration between several individuals across Google Research and Google Cloud, including (in alphabetical order): Pranjal Awasthi, Dawei Jia, Weihao Kong, Andrew Leach, Shaan Mathur, Petros Mol, Shuxin Nie, Ananda Theertha Suresh, and Rose Yu.

[ad_2]

Source link

best india pharmacy: india online pharmacy – top online pharmacy india

https://medicinefromindia.store/# top 10 online pharmacy in india

top 10 pharmacies in india

medicine in mexico pharmacies mexican pharmacy mexican pharmacy

п»їbest mexican online pharmacies mexican pharmaceuticals online buying from online mexican pharmacy

best online pharmacies in mexico mexican rx online medicine in mexico pharmacies

Lumiere — новый клубный квартал премиум-класса между Ильинским и Новорижским шоссе, в 9 км от Москвы.

mexico pharmacies prescription drugs mexico drug stores pharmacies mexico pharmacies prescription drugs

reputable mexican pharmacies online п»їbest mexican online pharmacies buying from online mexican pharmacy

mexican border pharmacies shipping to usa mexican online pharmacies prescription drugs mexico drug stores pharmacies

mexican pharmaceuticals online mexico drug stores pharmacies buying from online mexican pharmacy

https://mexicanph.com/# pharmacies in mexico that ship to usa

mexican online pharmacies prescription drugs

reputable mexican pharmacies online mexico pharmacies prescription drugs mexico drug stores pharmacies

mexico drug stores pharmacies п»їbest mexican online pharmacies mexican pharmacy

best online pharmacies in mexico best online pharmacies in mexico mexican border pharmacies shipping to usa

п»їbest mexican online pharmacies buying prescription drugs in mexico mexican border pharmacies shipping to usa

mexico pharmacy pharmacies in mexico that ship to usa buying from online mexican pharmacy

http://mexicanph.shop/# mexican border pharmacies shipping to usa

mexican pharmaceuticals online

mexico drug stores pharmacies mexican pharmacy best online pharmacies in mexico

buying prescription drugs in mexico online mexican drugstore online medication from mexico pharmacy

mexico drug stores pharmacies mexican mail order pharmacies purple pharmacy mexico price list

purple pharmacy mexico price list mexican pharmaceuticals online mexican pharmacy

mexican drugstore online medication from mexico pharmacy п»їbest mexican online pharmacies

mexican mail order pharmacies buying prescription drugs in mexico medicine in mexico pharmacies

п»їbest mexican online pharmacies buying prescription drugs in mexico reputable mexican pharmacies online

п»їbest mexican online pharmacies mexico pharmacy best online pharmacies in mexico

mexican online pharmacies prescription drugs mexican rx online mexican rx online

reputable mexican pharmacies online mexico pharmacy mexico pharmacy

order amoxicillin online: amoxicillin for sale online – amoxicillin online no prescription

stromectol ivermectin tablets: stromectol ivermectin 3 mg – price of ivermectin

http://furosemide.guru/# buy furosemide online

stromectol pill: stromectol xl – ivermectin 1% cream generic

ivermectin over the counter: ivermectin 0.5 lotion india – ivermectin where to buy for humans

generic lisinopril 3973: lisinopril pill 20mg – lisinopril 5mg cost

stromectol nz: stromectol tab price – п»їwhere to buy stromectol online

stromectol tablet 3 mg: stromectol tablets for humans for sale – ivermectin 4

ivermectin nz: stromectol online canada – stromectol south africa

lisinopril 20 mg: buy lisinopril online canada – cheap lisinopril 40 mg

lasix 100 mg: Buy Lasix No Prescription – furosemide 100 mg

ivermectin humans: ivermectin 5 – ivermectin lotion cost

lisinopril cost: zestril 10 mg cost – lisinopril 12.5 tablet

cheap amoxicillin 500mg: generic for amoxicillin – order amoxicillin online

where to buy lisinopril without prescription: lisinopril 1.25 mg – lisinopril 20mg discount

can i buy lisinopril over the counter in canada: lisinopril 120 mg – lisinopril 10 mg

buy furosemide online: Buy Lasix No Prescription – furosemide 100mg

buy zestril: lisinopril 30 mg price – lisinopril brand name cost

lisinopril 20g: zestril 10 mg price – 16 lisinopril

zestril 5 mg price: price for 5 mg lisinopril – lisinopril uk

amoxacillian without a percription: amoxicillin 200 mg tablet – buy cheap amoxicillin

lasix side effects: Buy Furosemide – lasix 100 mg

zestoretic 20 25: lisinopril 20 12.5 mg – zestril discount

prednisone 5mg price: cheapest prednisone no prescription – 200 mg prednisone daily

amoxicillin 500mg tablets price in india: amoxicillin 825 mg – purchase amoxicillin online without prescription

buy amoxicillin 500mg usa: amoxicillin 500mg price in canada – where can you get amoxicillin

canadian pharmacies viagra canadian pharmacies generic ed medication

viagra pharmacy online [url=http://canadianphrmacy23.com/]canadian pharmacies[/url]

cheapest online pharmacy india Online medicine order indianpharmacy com

top 10 pharmacies in india india pharmacy Online medicine home delivery

Online medicine home delivery top 10 online pharmacy in india buy medicines online in india

buy cytotec in usa: buy cytotec over the counter – cytotec buy online usa

diflucan online paypal: diflucan over the counter uk – where to buy diflucan in singapore

tamoxifen pill: tamoxifen buy – nolvadex side effects

Hello, World!

Hey there, mate! Greetings from your favorite surfing capybara!

How’s the surf today?

Ready to catch some gnarly waves together?

https://capybara888.wordpress.com/

Good luck!

ciprofloxacin 500mg buy online: antibiotics cipro – purchase cipro

where to purchase doxycycline: doxycycline monohydrate – doxycycline 100 mg

lana rhoades filmleri: lana rhoades izle – lana rhoades modeli

?????? ????: Angela White video – Angela Beyaz modeli

eva elfie izle: eva elfie – eva elfie

Angela White video: abella danger filmleri – abella danger filmleri

eva elfie filmleri: eva elfie filmleri – eva elfie izle

lana rhoades: lana rhoades modeli – lana rhoades video

Angela White filmleri: abella danger video – Abella Danger

eva elfie video: eva elfie filmleri – eva elfie video

eva elfie modeli: eva elfie filmleri – eva elfie modeli

Angela White filmleri: Angela White izle – ?????? ????

Angela White: abella danger izle – abella danger video

sweeti fox: swetie fox – sweety fox

https://evaelfie.site/# eva elfie full videos

https://sweetiefox.pro/# sweetie fox

https://sweetiefox.pro/# sweetie fox video

http://evaelfie.site/# eva elfie hot

https://miamalkova.life/# mia malkova hd

https://miamalkova.life/# mia malkova full video

http://evaelfie.site/# eva elfie

https://lanarhoades.pro/# lana rhoades boyfriend

lana rhoades pics: lana rhoades videos – lana rhoades pics

https://evaelfie.site/# eva elfie

http://lanarhoades.pro/# lana rhoades pics

http://lanarhoades.pro/# lana rhoades pics

http://evaelfie.site/# eva elfie photo

jogo de aposta: aviator jogo de aposta – jogos que dao dinheiro

https://aviatormocambique.site/# aviator

https://jogodeaposta.fun/# jogo de aposta online

http://aviatorghana.pro/# aviator game

https://pinupcassino.pro/# pin up casino

aviator betano: aviator betano – estrela bet aviator

buy generic zithromax online: over the counter zithromax where can i get zithromax over the counter

zithromax 250 mg: zithromax diarrhea can you buy zithromax over the counter in mexico

zithromax capsules: buy zithromax online fast shipping – zithromax capsules australia

indian pharmacies safe: india pharmacy – reputable indian pharmacies indianpharm.store

canadian online pharmacy: My Canadian pharmacy – canadian pharmacy canadianpharm.store

http://canadianpharmlk.shop/# legitimate canadian mail order pharmacy canadianpharm.store

http://indianpharm24.shop/# online shopping pharmacy india indianpharm.store

http://mexicanpharm24.com/# mexico drug stores pharmacies mexicanpharm.shop

https://indianpharm24.com/# Online medicine home delivery indianpharm.store

http://indianpharm24.com/# online shopping pharmacy india indianpharm.store

http://canadianpharmlk.com/# buy prescription drugs from canada cheap canadianpharm.store

https://indianpharm24.com/# best online pharmacy india indianpharm.store

http://canadianpharmlk.com/# reliable canadian pharmacy canadianpharm.store

http://canadianpharmlk.shop/# vipps approved canadian online pharmacy canadianpharm.store

https://canadianpharmlk.com/# reliable canadian pharmacy canadianpharm.store

https://mexicanpharm24.shop/# pharmacies in mexico that ship to usa mexicanpharm.shop

http://clomidst.pro/# buy generic clomid

https://prednisonest.pro/# prednisone 2.5 mg

http://amoxilst.pro/# where can i buy amoxicillin over the counter

https://amoxilst.pro/# amoxicillin online canada

https://clomidst.pro/# can you buy clomid without insurance

http://prednisonest.pro/# 20 mg prednisone tablet

http://onlinepharmacy.cheap/# legit non prescription pharmacies

http://pharmnoprescription.pro/# buy medications without prescriptions

https://edpills.guru/# cheapest online ed meds

https://edpills.guru/# buy erectile dysfunction treatment

http://edpills.guru/# best ed meds online

http://pharmacynoprescription.pro/# buying prescription drugs online canada

http://canadianpharm.guru/# canadian pharmacies compare

http://indianpharm.shop/# online pharmacy india

https://pharmacynoprescription.pro/# no prescription on line pharmacies

http://indianpharm.shop/# indian pharmacy paypal

https://pharmacynoprescription.pro/# buy medication online without prescription

http://canadianpharm.guru/# canadian world pharmacy

https://pharmacynoprescription.pro/# ordering prescription drugs from canada

https://canadianpharm.guru/# canadian pharmacy

https://canadianpharm.guru/# canadianpharmacymeds

http://indianpharm.shop/# mail order pharmacy india

https://canadianpharm.guru/# my canadian pharmacy review

http://mexicanpharm.online/# mexico pharmacy

https://canadianpharm.guru/# canadian mail order pharmacy

http://indianpharm.shop/# Online medicine order

pin up casino giris: pin up giris – pin up casino giris

pin-up online: pin up giris – pin up

aviator oyna slot: aviator oyunu 50 tl – aviator hilesi ucretsiz

casino slot siteleri: slot casino siteleri – slot siteleri bonus veren

slot kumar siteleri: casino slot siteleri – slot siteleri 2024

gates of olympus demo: gates of olympus demo oyna – gates of olympus demo turkce oyna

slot siteleri: yasal slot siteleri – bonus veren casino slot siteleri

sweet bonanza bahis: sweet bonanza yorumlar – sweet bonanza yasal site

slot siteleri guvenilir: en iyi slot siteleri 2024 – en cok kazandiran slot siteleri

online shopping pharmacy india: Cheapest online pharmacy – best online pharmacy india

best online pharmacies in mexico: Online Pharmacies in Mexico – mexican pharmacy

top online pharmacy india: Healthcare and medicines from India – indian pharmacy

Online medicine home delivery: indian pharmacy – best india pharmacy

https://sildenafiliq.com/# viagra without prescription

https://kamagraiq.shop/# Kamagra 100mg price

http://kamagraiq.shop/# super kamagra

http://sildenafiliq.xyz/# best price for viagra 100mg

Приветствую. Подскажите, где почитатьразные статьи о недвижимости? Пока нашел https://417-017.ru

Приветствую. Подскажите, где почитатьразные статьи о недвижимости? Пока нашел https://aquatopnn.ru

Приветствую. Подскажите, где почитатьразные блоги о недвижимости? Пока нашел https://artem-dvery.ru

Приветствую. Подскажите, где найтиполезные блоги о недвижимости? Сейчас читаю https://asiatreid.ru

Всем привет! Подскажите, где почитатьполезные статьи о недвижимости? Сейчас читаю https://dilerskiy-tsentr-baumit.ru

Приветствую. Может кто знает, где найтиразные блоги о недвижимости? Сейчас читаю https://dompodkluch33.ru

Приветствую. Может кто знает, где найтиразные статьи о недвижимости? Пока нашел https://eniseyburvod.ru

Всем привет! Подскажите, где найтиразные статьи о недвижимости? Пока нашел https://etalon-voda.ru

Всем привет! Может кто знает, где почитатьразные блоги о недвижимости? Пока нашел https://floor-ashton.ru

Всем привет! Может кто знает, где найтиполезные блоги о недвижимости? Пока нашел https://gismt72.ru

Всем привет! Подскажите, где почитатьразные статьи о недвижимости? Пока нашел https://kait-volga.ru

Приветствую. Может кто знает, где найтиразные блоги о недвижимости? Пока нашел https://kaluga-elite.ru

Всем привет! Может кто знает, где почитатьполезные блоги о недвижимости? Пока нашел https://kamenolomnya43.ru

Всем привет! Подскажите, где найтиразные блоги о недвижимости? Сейчас читаю https://kmzperm.ru

Всем привет! Может кто знает, где найтиполезные статьи о недвижимости? Сейчас читаю https://kovry159.ru

Приветствую. Может кто знает, где найтиразные блоги о недвижимости? Сейчас читаю https://krepegmaster.ru

Привет Друзья!

Всегда думал что купить диплом о высшем образовании это миф и нереально, но все оказалось не так, изначально искал информацию про: купить диплом техникума, купить диплом в серове, купить диплом с реестром, купить диплом в новомосковске, купить диплом в белгороде, потом про дипломы вузов, подробнее здесь https://crossbookmark.com/story17260313/%D0%BF%D0%BE%D0%BB%D1%83%D1%87%D0%B8%D0%BB-%D0%B4%D0%B8%D0%BF%D0%BB%D0%BE%D0%BC-%D0%BF%D0%BE%D0%B7%D0%B4%D1%80%D0%B0%D0%B2%D0%BB%D1%8F%D1%8E

Оказалось все возможно, официально со специальными условия по упрощенным программам, так и сделал и теперь у меня есть диплом вуза Москвы нового образца, что советую и вам!

Хорошей учебы!

Всем привет! Подскажите, где почитатьполезные блоги о недвижимости? Пока нашел https://kuler-tsentr.ru

Всем привет! Может кто знает, где почитатьполезные статьи о недвижимости? Сейчас читаю https://liem-com.ru

Всем привет! Подскажите, где найтиполезные статьи о недвижимости? Сейчас читаю https://oscltd.ru

Всем привет! Подскажите, где найтиразные статьи о недвижимости? Сейчас читаю https://ppu-odk.ru

Всем привет! Может кто знает, где найтиразные статьи о недвижимости? Сейчас читаю https://redglade-nn.ru

Всем привет! Подскажите, где почитатьполезные блоги о недвижимости? Пока нашел https://santam1.ru

Всем привет! Может кто знает, где почитатьполезные статьи о недвижимости? Сейчас читаю https://sibarit54.ru

Приветствую. Подскажите, где почитатьразные статьи о недвижимости? Пока нашел https://stroyproektm.ru

Приветствую. Может кто знает, где почитатьразные статьи о недвижимости? Пока нашел https://tent44.ru

Всем привет! Может кто знает, где найти разные статьи о недвижимости? Пока нашел https://1eve1.ru

Приветствую. Может кто знает, где почитать разные статьи о недвижимости? Пока нашел https://an72.ru

Приветствую. Может кто знает, где почитать разные блоги о недвижимости? Пока нашел https://armid44.ru

Приветствую. Подскажите, где найти разные статьи о недвижимости? Сейчас читаю https://azimut-irkutsk.ru

Всем привет! Может кто знает, где почитать полезные статьи о недвижимости? Пока нашел https://ecn-novodom.ru

Всем привет! Может кто знает, где найти разные статьи о недвижимости? Пока нашел https://germes-alania.ru

Приветствую. Подскажите, где почитать полезные блоги о недвижимости? Пока нашел https://ilinka2.ru

Всем привет! Может кто знает, где найти полезные блоги о недвижимости? Пока нашел https://kolontaevo-club.ru

Приветствую. Может кто знает, где почитать полезные статьи о недвижимости? Пока нашел https://mcsspb.ru

Всем привет! Может кто знает, где найти разные блоги о недвижимости? Пока нашел https://officesaratov.ru

Приветствую. Подскажите, где найти полезные блоги о недвижимости? Пока нашел https://sintes21.ru

Всем привет! Подскажите, где почитать полезные статьи о недвижимости? Сейчас читаю https://ste96.ru

Приветствую. Подскажите, где найти разные статьи о недвижимости? Пока нашел https://kran-rdk.ru

Всем привет! Подскажите, где найти полезные статьи о недвижимости? Сейчас читаю https://mart-posters.ru

Приветствую. Подскажите, где почитать разные блоги о недвижимости? Сейчас читаю https://tochkacn.ru

Всем привет! Может кто знает, где найти разные статьи о недвижимости? Сейчас читаю https://metrazhi-omsk.ru

Приветствую. Подскажите, где найти разные статьи о недвижимости? Сейчас читаю https://mik-dom.ru

Всем привет! Подскажите, где почитать полезные статьи о недвижимости? Пока нашел https://miro-teh-ural.ru

Всем привет! Может кто знает, где почитать полезные блоги о недвижимости? Пока нашел https://mzhk-stroy.ru

Всем привет! Может кто знает, где найти разные статьи о недвижимости? Пока нашел https://nagaevodom.ru

Всем привет! Может кто знает, где почитать полезные статьи о недвижимости? Пока нашел https://potolkinomer1.ru

Приветствую. Может кто знает, где почитать полезные блоги о недвижимости? Пока нашел https://promresmag.ru

Всем привет! Подскажите, где найти разные блоги о недвижимости? Пока нашел https://santech31.ru

Всем привет! Подскажите, где почитать разные блоги о недвижимости? Сейчас читаю https://santex-expert.ru

Приветствую. Может кто знает, где найти разные статьи о недвижимости? Пока нашел https://schuconvr.ru

Приветствую. Подскажите, где почитать полезные блоги о недвижимости? Сейчас читаю https://simposad.ru

Приветствую. Может кто знает, где найти разные статьи о недвижимости? Сейчас читаю https://smgarant.ru

Всем привет! Может кто знает, где найти разные статьи о недвижимости? Пока нашел https://stilnyjpol.ru

Приветствую. Может кто знает, где почитать полезные статьи о недвижимости? Пока нашел https://tc-all.ru

Всем привет! Подскажите, где найти полезные блоги о недвижимости? Пока нашел https://teplohod-denisdavidov.ru

Всем привет! Может кто знает, где найти разные блоги о недвижимости? Сейчас читаю https://titovloft.ru

Приветствую. Подскажите, где найти полезные статьи о недвижимости? Сейчас читаю https://toadmarket.ru

Всем привет! Может кто знает, где найти разные блоги о недвижимости? Пока нашел https://u-mechanik.ru

Всем привет! Может кто знает, где почитать разные блоги о недвижимости? Пока нашел https://utc96.ru

Приветствую. Может кто знает, где найти разные блоги о недвижимости? Сейчас читаю https://vortex-los.ru

Всем привет! Подскажите, где почитать полезные блоги о недвижимости? Пока нашел https://yah-bomag.ru

Всем привет! Может кто знает, где почитать разные статьи о недвижимости? Сейчас читаю https://yaoknaa.ru

Приветствую. Подскажите, где найти полезные блоги о недвижимости? Пока нашел https://zt365.ru

Приветствую. Подскажите, где найти разные статьи о недвижимости? Сейчас читаю https://astali.ru

Приветствую. Может кто знает, где почитать полезные блоги о недвижимости? Сейчас читаю https://batstroimat24.ru

Всем привет! Подскажите, где почитать полезные блоги о недвижимости? Пока нашел https://bdrsu-2.ru

Приветствую. Может кто знает, где почитать полезные статьи о недвижимости? Сейчас читаю https://centro-kraska.ru

Приветствую. Может кто знает, где найти полезные блоги о недвижимости? Сейчас читаю https://cvetkrovli.ru

Всем привет! Подскажите, где найти разные блоги о недвижимости? Пока нашел https://deon-stroy.ru

Для тех, кто хочет наслаждаться всеми возможностями мобильного беттинга без затрат, скачать Фонбет на айфон бесплатно – отличное решение. Приложение Фонбет предоставляет пользователям удобный интерфейс, быстрый доступ к различным спортивным событиям и возможность делать ставки в любое время и в любом месте. Скачайте Фонбет на айфон бесплатно и получайте удовольствие от ставок.

Всем привет! Может кто знает, где почитать разные статьи о недвижимости? Сейчас читаю https://dom-vasilevo.ru

Всем привет! Может кто знает, где почитать полезные статьи о недвижимости? Сейчас читаю https://2204000.ru

Всем привет! Подскажите, где найти полезные статьи о недвижимости? Пока нашел https://adeldv.ru

Приветствую. Подскажите, где почитать полезные статьи о недвижимости? Пока нашел https://eniseynev.ru

Приветствую. Подскажите, где найти полезные блоги о недвижимости? Сейчас читаю https://fuseitdecore.ru

Приветствую. Подскажите, где почитать разные статьи о недвижимости? Сейчас читаю https://galastroy-sk.ru

Всем привет! Может кто знает, где найти разные блоги о недвижимости? Пока нашел https://ggs45.ru

Всем привет! Может кто знает, где почитать разные блоги о недвижимости? Сейчас читаю https://glwin.ru

Всем привет! Может кто знает, где найти разные статьи о недвижимости? Пока нашел https://gor-bur.ru

Приветствую. Подскажите, где найти разные блоги о недвижимости? Сейчас читаю https://hameleon1.ru

Приветствую. Подскажите, где почитать разные блоги о недвижимости? Пока нашел https://iskrb.ru

Приветствую. Подскажите, где найти полезные блоги о недвижимости? Пока нашел https://juzhnybereg24.ru

Приветствую. Подскажите, где найти полезные статьи о недвижимости? Пока нашел https://klimat-hck.ru

Зарегистрируйтесь на сайте Пари и активируйте БК Пари промокод, чтобы получить эксклюзивные бонусы и скидки на ставки. Увеличьте свои шансы на победу!

Всем привет! Может кто знает, где найти разные статьи о недвижимости? Сейчас читаю https://kolahouse.ru

Всем привет! Подскажите, где найтиразные блоги о недвижимости? Сейчас читаю https://sm70.ru

Приветствую. Подскажите, где найти разные статьи о недвижимости? Сейчас читаю https://komdizrem.ru

Приветствую. Подскажите, где найти полезные блоги о недвижимости? Пока нашел https://konditsioneri-shop.ru

Всем привет! Подскажите, где почитать разные блоги о недвижимости? Пока нашел https://glatt-nsk.ru

Приветствую. Может кто знает, где найти полезные статьи о недвижимости? Пока нашел блог о недвижимости

Приветствую. Подскажите, где почитать полезные блоги о недвижимости? Сейчас читаю https://glatt-nsk.ru

Всем привет! Подскажите, где почитать полезные статьи о недвижимости? Сейчас читаю https://gor-bur.ru

Приветствую. Может кто знает, где найти полезные статьи о недвижимости? Сейчас читаю https://konditsioneri-shop.ru